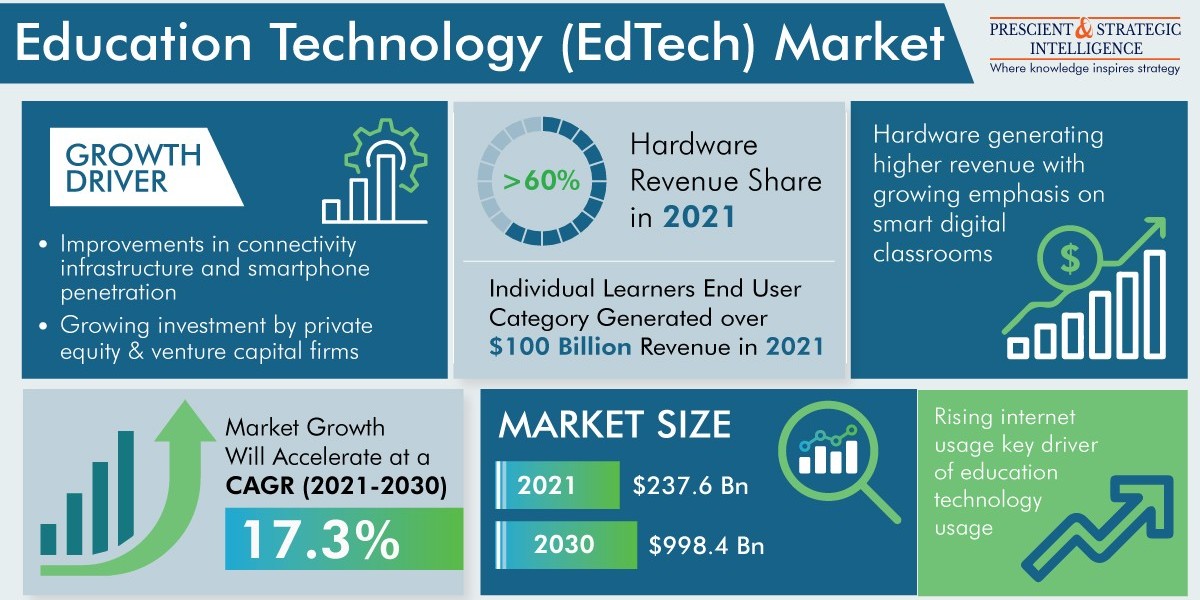

In 2021, the edtech market hit $237.6 billion revenue, and it is expected to advance at a rate of 17.3% from 2021 to 2030, to reach $998.4 billion by 2030. This is chiefly attributed to the increased emergence of the artificial intelligence and digitalization in the edtech industry. Advanced technologies such as IoT and the incorporation of augmented reality and virtual reality facilitate the enhanced interactive learning experience for students resulting in the market boom.

The impact of the COVID-19 with the announced lockdown by governments worldwide has resulted in the booming of the education technology market, attributed to the increased demand for EdTech solutions. The situation highlighted the potential of the advanced education technologies to facilitate remote learning resulting in a market boost. The market players are focusing on expanding product offerings to offer interrupted learning.

APAC holds the most-significant share in the edtech market, of 45%, attributed to the rising internet penetration led by smart devices. The financial aid provided by governments to digitalize education has also resulted in market proliferation. Developing countries such as India and China have invested in facilitating the accessibility of digital devices to students, resulting in market expansion. For example, the Indian government placed around 20,000 digital boards in Delhi.

Moreover, the emergence of advanced technologies, the rising number of vendors facilitating remote learning services, and the surge in students leads to edtech market expansion. Furthermore, the worldwide most expensive education system belongs to China, with the presence of around 500,000 schools, 280 million students, and 18 million teachers.

North America is the next significant contributor after APAC to the edtech market, holding a 20% revenue share, attributed to the high investments made in the education sector in India and increased participation of companies aiming to expand the geographical reach to cater to large customer base. For example, Class Technologies raised more than $100 million in the B series funding to expand geographically outside the U.S.

Under the type segment, hardware is the most significant contributor to the edtech market, amounting to 60% of revenue, attributed to the increased sales in the emerging economies. The booming sales of hardware equipment such as interactive displays, laptops, tabs, and secure digital (SD) cards propel the market. Tabs have witnessed massive sales, followed by laptops. The Apple Inc. contributed significantly to the sales of tabs amounting to 40%, leaving behind its competitors such as Samsung Electronics Co. Ltd., Amazon.com Inc. and Lenovo Group Ltd.

The growing popularity of digital classrooms propels the education technology market, ascribed to increased hardware demand. The key players aim to expand the digital classroom platforms, attributed to the rising importance of digital classrooms. For example, in February 2022, VR headsets were offered to Smt. GDS Sr. Sec. School by Veative Labs, in India to facilitate the virtual learning experience to students in subjects such as Science.

Under the end user segment, individual learners are contributing majorly to the market growth, generating over $100 billion in revenue in 2021, attributed to the inclination toward acquiring new skills and high budget allocation in the education sector. For example, the Indian Union Budget allocated INR 1,04,278 crore to the education sector for the 2022–2023 session. The rising investment to enhance digital connectivity to facilitate high-quality education resulted in the market boom.

Therefore, the COVID19 lockdown and increased popularity of digital classrooms with advanced learning solutions have resulted in boosting the market.