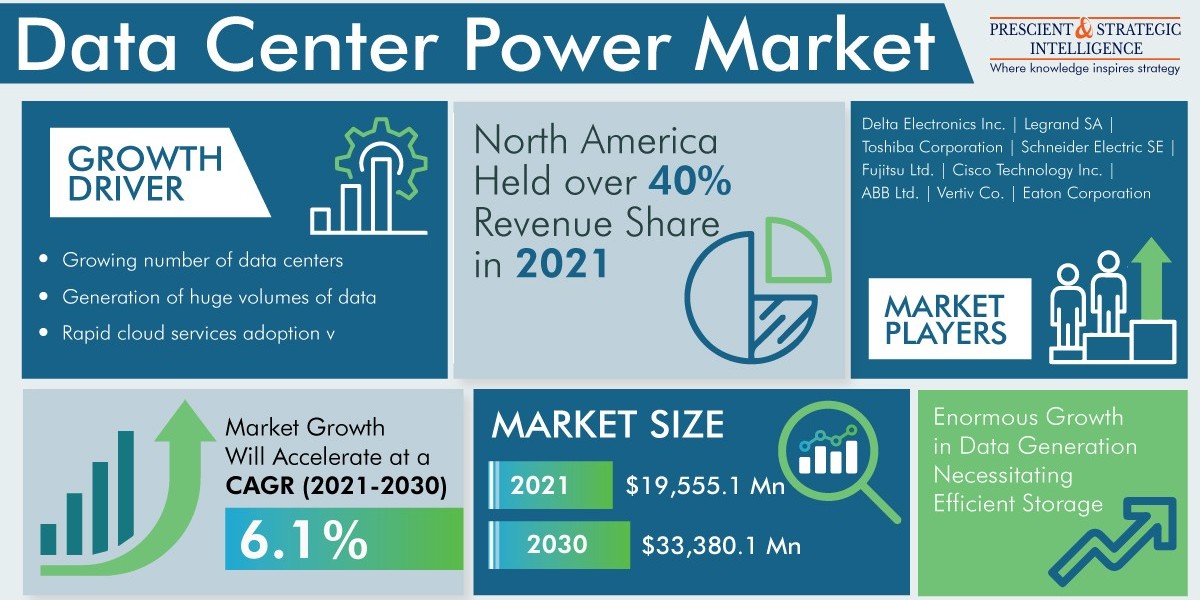

The prominent factors thriving the global data center power market are robust adoption of cloud solutions, generation of a huge amount of data, and an increase in the number of data centers. In 2021, the market stood at $19,555.1 million and it is projected to touch $33,380.1 million by 2030. Moreover, the market is projected to advance at a CAGR of 6.1% from 2021 to 2030, owing to the huge requirement of entrepreneurs to drift to data centers from server rooms, the surge in smartphone penetration, the rise in social media usage, and the increase in the count of internet users.

In 2021, the tier III & tier IV category ruled the data center power market, holding approximately 90% of the total revenue share, and this trend will continue in the forecast period as well. This can be credited to its unique features, which include providing the N+1 and 2N redundancy, implying that the complete IT load can be assisted by the structure, simultaneously encompassing additional equipment for power backup, so that the execution is not hampered even if any part fails. The redundant systems ensure the smooth functioning of the performance during any failure.

Within the equipment type, the data center power market will witness a skyrocketing demand for UPS systems because of safeguarding critical components across a facility and maintaining continuity in the functioning of larger data centers. They comprise dual-bus capabilities and multiple configurations to confirm the working of critical systems during power blackouts and outbursts. To converge with the critical component’s power needs, the control system and modular creation of a completely redundant power can be sized by the UPS systems. For any changes in the power requirements, the simple inclusion of the capacity will work.

Based on vertical, the IT and telecommunications category will dominate the data center power market in the coming years. This can be ascribed to the generation of voluminous data due to an elaborated use of the latest technologies, including AI, cloud computing, and IoT. The sources of this data include social networks, billing activities, server logs, network equipment, and personnel records. This data needs to be aptly analyzed to make business decision and improve customer services.

The swiftly expanding data generation is exhibiting enormous growth in the data center power market by facilitating efficient storage. Approximately 64.2 zettabytes of data were generated in 2020, which increased by 314% as compared to 2015. Moreover, 2.5 quintillion bytes of data are accumulated across the world every single day. Almost 90% of the global data was created in the past 4–5 years, with the incorporation of social media platforms and IoT. This is major because of the surging usage of IoT, embedded, and machine-to-machine devices.

In 2021, North America held the largest revenue share in the data center power market. This is attributed to the significant spending on R&D activities in this region, which further pushes the formation of next-generation facilities, which are efficient in managing power and technologically advanced. Being home to many data center developers, the region will witness significant market growth. However, APAC will be the fastest-growing market in the forecast period because several regional countries, such as China, Japan, and India, have integrated edge computing locations.

Hence, an escalating count of data centers, coupled with a dire requirement of entrepreneurs to drift to data centers from server rooms will drive the market.

Source: P&S Intelligence